US housing starts are slowing, reducing future supply and giving apartment owners a clearer path to stronger rent growth by 2027.

via Jordan B via CRE Daily <— Click here for similar articles

- US housing starts fell to their lowest level since 2020, pointing to fewer new homes reaching the market over the next two years.

- Builders are delaying projects and adopting build-to-order strategies, limiting near-term competition for apartment operators despite weak new-home demand.

- Marcus & Millichap expects the slowing supply pipeline to help multifamily owners reduce concessions and regain pricing power as recent deliveries are absorbed.

- Dreznin Pappas Commercial Real Estate LLC also sees a slowdown in construction on the Gulf Coast of Florida which has reduced new supply and helped the market digest the previous new supply delivered. Vacancy is still elevated and concessions are still part of today’s rental markets, but we seem to have a solid floor in our rearview mirror.

For multifamily investors, the biggest story in housing may be what is no longer getting built. According to Marcus & Millichap’s July 2026 housing analysis, builders are pulling back as demand remains uneven. That slowdown should reduce new housing supply through at least 2027, giving apartment owners more time to absorb the record wave of recent deliveries.

Residential Construction Loses Momentum

The housing market has shifted from rapid expansion to cautious restraint. Builders are delaying projects instead of pushing ahead with speculative construction. Marcus & Millichap says the share of homes listed for sale but not yet under construction reached a record high in May. The trend reflects a growing preference for build-to-order development, allowing builders to limit risk until buyer demand improves. For apartment operators, fewer new for-sale homes could keep more households in the rental market over the next several years.

Source: Marcus & Millichap

The Details

The broader construction pipeline continues to weaken. Marcus & Millichap reports total US housing starts fell to an annualized 1.18M units in May. That marked the lowest monthly reading since April 2020. Single-family completions also declined 16.8% year over year, reaching their lowest level since mid-2020.

Demand remains soft despite rising inventory. New-home sales fell to a seasonally adjusted annual rate of 580,000 in May, the second-lowest level in the past three years. Meanwhile, months of supply climbed to 10.3, the highest reading since mid-2022. Those conditions have encouraged builders to preserve flexibility instead of accelerating construction.

Multifamily Rent Growth Outlook Improves

Apartment owners are still working through elevated supply in many markets. Nationwide rent concessions remained near 11% in May, according to Marcus & Millichap. A slower development pipeline could gradually change that equation.

With fewer homes entering the market, multifamily operators may gain room to reduce incentives as existing inventory leases up. The firm expects declining residential deliveries to ease competitive pressure through at least 2027. That should create healthier conditions for rent growth after several years of supply-driven pricing challenges.

Existing-home activity also offers modest encouragement. Sales increased 3.3% year over year in May. First-time buyers accounted for 35% of transactions, up from 30% a year earlier.

Why It Matters

Housing and multifamily markets remain closely connected. When home construction slows, apartment operators typically face less competition from new ownership inventory. That relationship becomes more important after the record apartment completions delivered across many Sun Belt and high-growth markets.

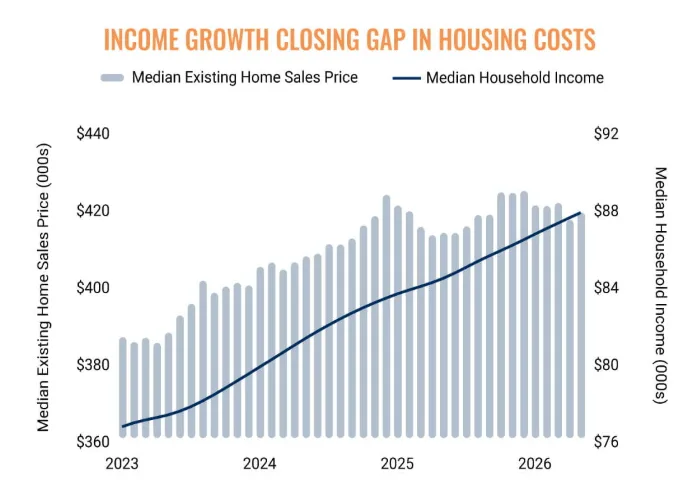

Marcus & Millichap also notes affordability has improved modestly. First-quarter wages increased 3.8% from a year earlier, while median existing-home prices have remained relatively flat since early 2025. Those trends could gradually strengthen housing demand without triggering another surge in new construction.

What’s Next

Investors will watch whether builders continue delaying projects through the second half of 2026. If housing starts remain subdued, apartment supply should continue tightening into 2027.

Interest rates remain another key variable. Marcus & Millichap says a more predictable borrowing environment could improve transaction activity across multifamily assets. However, persistent inflation or additional rate hikes would keep financing costs elevated and pressure underwriting, particularly in markets still digesting large volumes of new apartment supply.

Dreznin Pappas Commercial Real Estate LLC sees a similar future for multifamily and income producing commercial real estate which includes a positive path with delayed new projects or rate relief assisting the overall market momentum. If rates rise or inflation continues to stagnate or tick up, then those headwinds would likely add water to any potential spark or positivity for overall markets.

Leave a comment