By Jay Parsons – visit Jay’s website here <—-

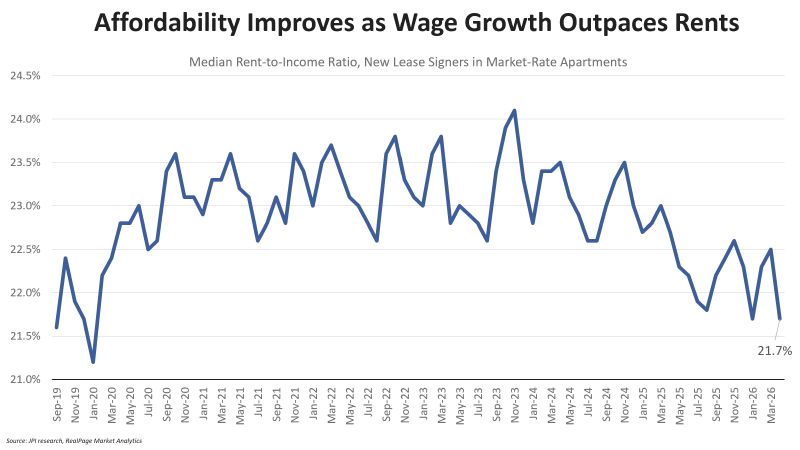

One of the U.S. apartment sector’s greatest tailwinds is something widely miscast as a headwind — affordability. Wage growth has outpaced new lease rent growth for 3+ years. Rent-to-income ratios nationally are down to the lowest levels since pre-COVID. And in earnings calls last week, public REITs reported rent-to-income ratios ranging from 19% to 22%.

How do we square this with all the headlines screaming about an affordability crisis?

Friendly reminder: Two things are true, even if seemingly conflicting, and it reflects a K-shaped economy of “haves” and “have nots” —

1) We do have a severe shortage of housing for low-income families, particularly for those making <$30k per year. Harvard research shows this group spends more than 80% of income on rent, which is indeed a real crisis. At those income levels, most families can’t afford to pay even the operating costs of a typical apartment without being rent burdened. This is a crisis indeed.

2) There’s also been ample demand for market-rate apartments among households who can afford it, spending (at median) 21.7% share of income on rent — well below the affordability ceiling of 30%. And it’s down from a peak of 24% in 2023. You can credit that improvement on the wave of nearly 1.5 million new apartments built between 2023-25, putting downward pressure on rents even as net absorption registered near record highs.

That data covers households signing a new lease in market-rate apartments, and we see similarly encouraging signs of renters renewing leases as well. REITs continue to report improved bad debt — meaning more renters are paying the rent — while resident retention continues to improve. In other words: Renters are renewing more often and paying the rent more often.

Camden’s Alex Jessett said that in Q1, “we recorded our lowest bad debt level since the onset of COVID-19 at less than 40 basis points.” Part of the reason for improved collections could be lower rent-to-income ratios (coupled with better initial screening) when they first sign a lease. UDR’s Michael Lacy said their rent-to-income ratios are better than the long-term average, “which suggests an encouraging outlook for renewal growth going forward.”

This data is a friendly reminder that painting renters in broad strokes is unhelpful. It distracts from the real issues at the low end of the market by misdirecting blame to the upper end of the market. To address affordability challenges in America, we need to zoom in on the segments of the market where those challenges exist.

But for the conventional apartment market overall, with some exceptions (particularly in the Class C market in some areas), affordability is becoming more of a tailwind than a headwind.

#multifamily #rent #affordability

Leave a comment