You have to appreciate this level of research and insights into the specific commercial real estate markets by Jay Parsons and RealPage. CLICK HERE for full article and others link it.

The FDIC issued an advisory this week that lumps multifamily in with office as potentially high-risk sectors. While there are certainly real risks, the pairing with office feels like a big oversell. Here’s why:

1) Unlike office, multifamily demand is healthy. Vacancy (while up) is back to the long-term average and showing signs of stabilizing. Absorption is still very healthy, even if “slowed” (in the FDIC’s wording) from 2021’s record pace.

2) Rents have cooled (not tanked) — and, unlike office’s demand challenges, it’s all about short-term supply for multifamily. That said, the FDIC’s memo used the word “overbuilding” — which is a bit wild because it’s contradicting the White House’s (correct) view that we’re still undersupplied, especially at the lower-rent levels. What the FDIC is really referring to is a short-term supply/demand imbalance that will almost certainly get corrected after 2024 due to 2023’s plunge in new starts.

Healthy demand + improving rent outlook should keep capital committed to multifamily and prevent a doomsday scenario.

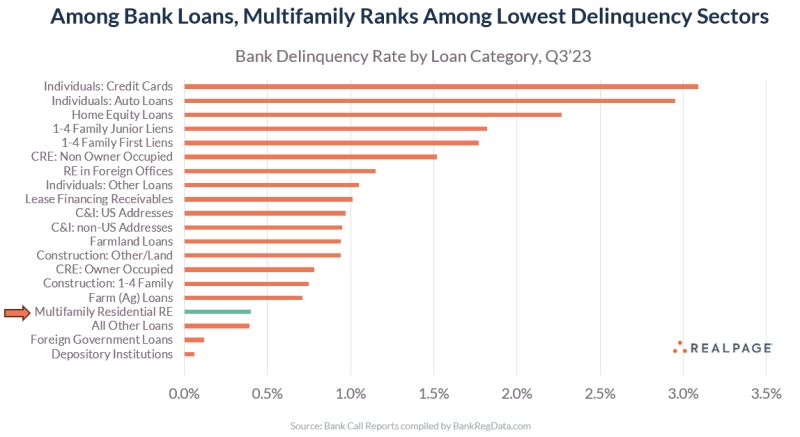

3) Multifamily bank loans have the lowest delinquency rate of all major bank lending categories, according to the latest quarterly filings from FDIC-insured banks – a key factoid left out of the FDIC’s memo. Multifamily delinquency came in at 0.40%, according to BankRegData. Other real estate categories were 2-3x higher. Delinquency will probably increase in 2024, but we’re starting at a very low point.

In fairness, rate risk is obviously a bigger concern than fundamentals. That’s especially true for those with short-term, floating rate debt. BUT that doesn’t represent the bulk of *bank* loans. Most are the more-vanilla, less-leverage variety.

Some might still get challenged maintaining required DSCRs, while still making payments — which is likely the type of profile banks would be motivated to work with. And even if not, it’s unlikely most properties would be worth less than the senior bank debt — further protecting banks.

Of course, it’s also important to acknowledge that a small share of banks will have more exposure to higher-risk multifamily through debt funds, bridge loans and CMBS they’re backing. Those smaller categories are not categorized with traditional multifamily loans in regulatory filings.

Another potential challenge for CRE/MF borrowers of all types: While the regulators continue to encourage lenders to pursue workouts as needed, the FDIC is also telling banks to preserve more capital — which means bank lending/refinancing could remain limited.

Those two strategies somewhat counteract each other. So there are real risks, yes, even for multifamily. But – unlike office – multifamily benefits from a broader lender pool outside the bank, starting with Fannie and Freddie. The agencies seem very in tune with their importance at this stage in the cycle; and while that’s no panacea, it’s another reason why multifamily is unlikely to play out like office.Activate to view larger image,

Here is a link to the FDIC’s advisory memo — > CLICK HERE <—-

Leave a comment