Ten-year CMBS conduit loans lost favor after 2022 as borrowers chose five-year debt, though spreads still support select deals.

By Valerija via CRE Daily <— Click Here for complete article

- Borrowers have shifted from 10-year to five-year CMBS conduit loans, with 10-year share dropping to just 12.3% of originations in 2026, according to Trepp.

- Despite spread tightening for 10-year loans across most property types, the longer-term structure is now reserved for properties with low leverage and strong cash flow.

- This marks a decisive break from the last CMBS cycle, as debt duration preferences reshape the risk calculus for both borrowers and investors.

Shorter Durations Take Hold

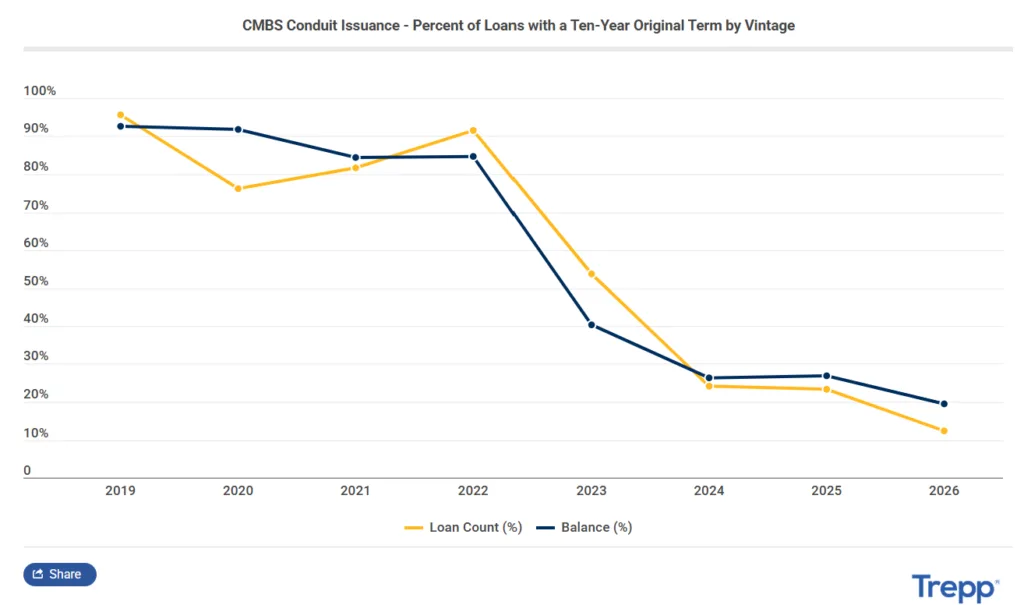

Borrowers are dumping the traditional 10-year conduit loan in favor of shorter, five-year executions, according to new Trepp data. For years, 10-year terms were the market default, preferred for their fixed-rate stability by both borrowers and CMBS investors. But since late 2022, volatility, higher base rates, and rising refinancing risks have altered the calculus. By mid-2026, 10-year conduit loans represented just 12.3% of new CMBS issue counts and 19.4% of balances—a sea change from their 95.6% share of originations in 2019.

This dramatic decline signals a structural shift in borrower preferences and risk appetite. Flexibility, not duration, now dominates CMBS decision-making, as investors and borrowers brace for continued rate and macroeconomic uncertainty. The five-year conduit loan, once a fringe product, has rapidly become the new industry standard.

Get Smarter about what matters in CRE

Connect with us at www.DP-CRE.com or email us directly at TritonCRE@gmail.com.

The End of the Decade-Long Default

As recently as 2022, the 10-year structure still accounted for more than 91% of loan counts and nearly 85% of conduit balances, per Trepp. The tide turned sharply in 2023—10-year loans plunged to 53.7% of issue count, continuing their collapse to 24.2% in 2024, and stabilizing around 23–24% in 2025 before reaching today’s single digits. In parallel, five-year loans filled the void, taking over as the dominant structure.

The post-pandemic rate environment has been the catalyst. With base rates climbing and future refinancing terms uncertain, CRE borrowers began to value optionality and flexibility over fixed-rate longevity. Many view locking in a decade-long loan as a bet they’d rather not place, especially if market conditions or property performance change in the interim.

Spreads Tighten, but Selectivity Rules

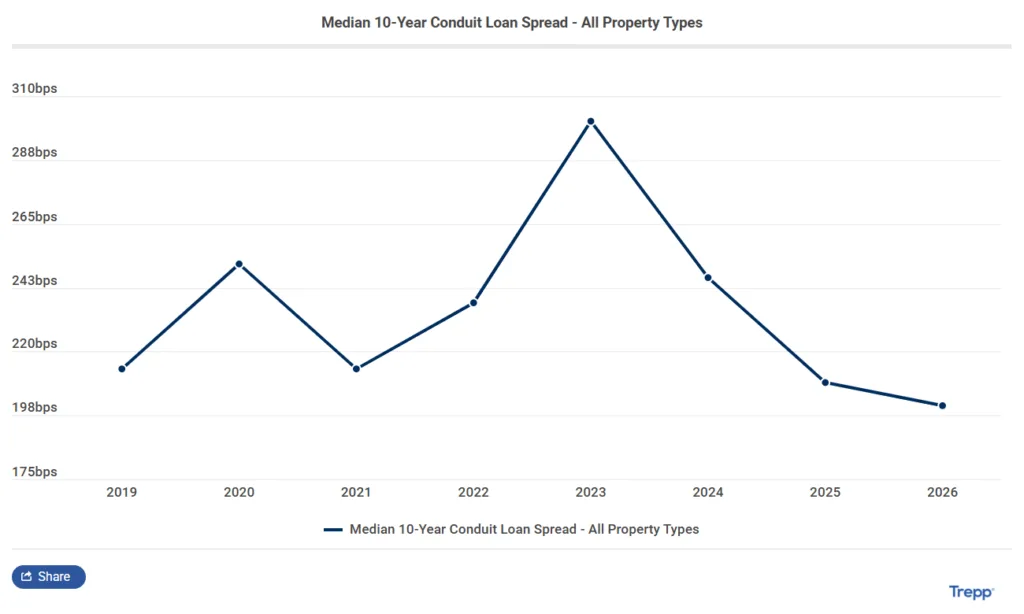

Crucially, this isn’t just a pricing story. While 10-year loan spreads ballooned to 301 basis points in 2023, they tightened significantly in subsequent years—down to 201 basis points by 2026, according to Trepp. Across asset classes, spreads retreated toward pre-pandemic levels, especially for assets with strong sponsorship and stable cash flows.

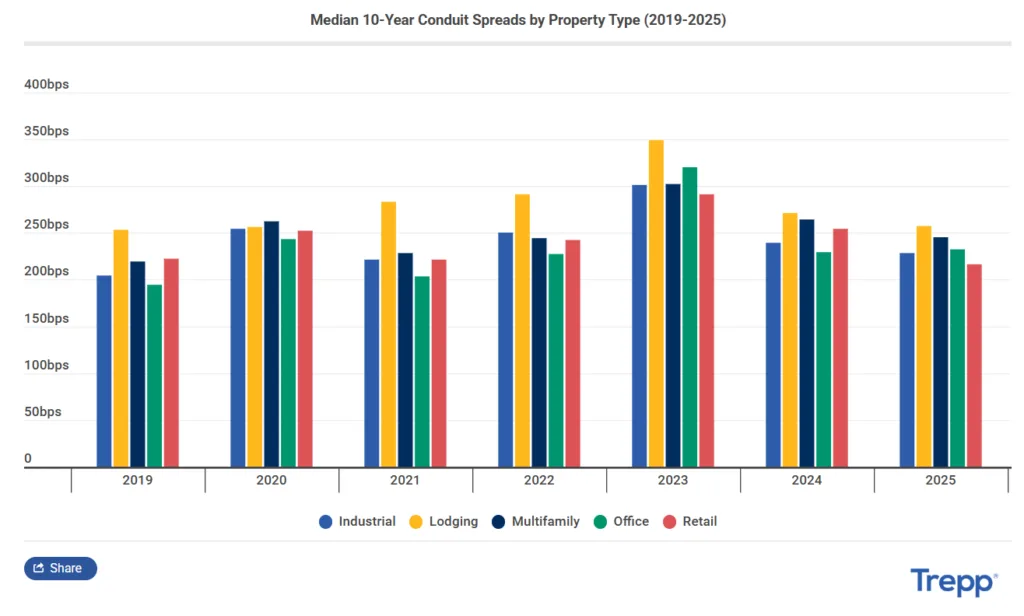

But the data also reveals a sharply selective lending environment. Lodging, traditionally more volatile, saw 10-year spreads peak at 349 basis points in 2023 before tightening to 257 in 2025. Office followed suit, with spreads rising to 320 basis points and then retreating to 232 in 2025. Only the best collateral—lower leverage, quality tenancy, market resilience—can clear the higher bar set for 10-year debt. For most assets, shorter terms are safer, especially in uncertain times.

Duration Preferences Recast Risk

Why does this matter? The rapid shift in duration preference points to an industry fundamentally rethinking risk and reward. The popularity of five-year executions reflects a deep borrower aversion to locking into decade-long commitments as rates remain unpredictable. Even as spreads on 10-year loans return to earth, originations remain rare—proof that underwriting discipline and sponsor quality now rule the day for long-term CMBS debt. That caution comes as office-backed CMBS faces a heavy wave of maturities in 2026, adding pressure to refinancing decisions. For borrowers, shorter terms allow for refinancing or repositioning if conditions improve. For lenders, it means less exposure to long-term macro shifts.

The changes are visible at the property-type level. Retail, for example, posted the tightest median spread for 10-year conduit loans by 2025 at 216 basis points, per Trepp, highlighting perceived durability in certain subsectors. Multifamily and industrial loans saw similar but less dramatic retracement, while lodging and office risk premiums remain elevated.

For the wider market, this tipping point signals the end of the 10-year loan as a default, and its rebirth as a niche product for best-in-class sponsors and assets—a return to disciplined, property-specific underwriting as the norm.

What’s Next

With 10-year conduit loans now a minority offering, all eyes are on how broader debt market and rate cycles evolve. If rates stabilize and economic clarity returns, investors may again favor longer-dated assets. For now, five-year loans dominate, and future CMBS issuance is likely to reflect this shorter-term orientation. Expect lenders to remain judicious, reserving 10-year executions for assets with the strongest credit profiles. And as data on 10-year loans thins, borrowers and lenders alike will need to adjust strategies to fit a market no longer built on decade-long debt.

Leave a comment