It’s been too long since I have referenced a Jay Parson’s research post so rest easy my friends, here is a golden article from Mr. Parson’s.

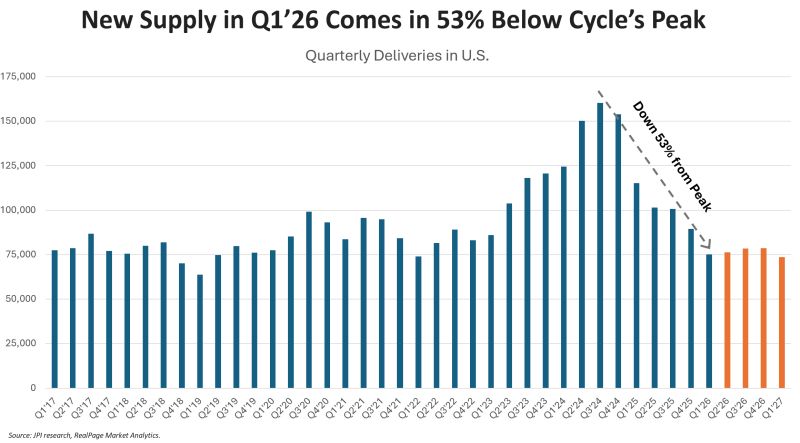

Apartment completions in Q1’26 totaled 75k units, a 53% drop from the cycle’s peak and one of the lowest tallies in seven years. Future deliveries are expected to come in around these levels through 2026 and into 2027, if not longer.

Apartment investors and operators have long awaited this storyline shift. Completions in 2023-24-25 marked the largest supply wave since the 1970s. While deliveries fell from 2024 to 2025, last year’s total was still higher than any year (other than 2023 and 2024) since the mid-1980s. It was a lot.

Some critical context to these numbers:

1) Supply is not evaporating altogether as occurred amidst the Great Financial Crisis and into the early 2010s. But it’s subsiding to more normal, absorbable levels. And on an inventory growth basis (% growth), the drop is even greater than the nominal numbers — coming in well below pre-pandemic norms in most markets.

2) We’re still working through the supply overhang from 2023-25. Many properties completing in that time frame are still working through lease-up with generous concessions, and therefore continuing to put downward pressure on rents across all price points in higher-supplied markets. Those pressures will likely continue until vacancy rates normalize.

3) Another consideration: Affordable housing comprises a larger-than-normal share of recent starts (and future completions). Pre-COVID, affordable comprised 10-12% of supply (according to Yardi). More recently, it’s closer to 20%. Workforce properties are a bigger share, too. That should likely mean further reduced supply pressures on the Class A market over time.

4) The supply drop-off is a national phenomenon. Not just in the Sun Belt and Mountain markets, which built heavily in this last cycle. But even in lower-supplied markets like the Midwest, thanks to debt costs and other headwinds.

Reminder: As noted above, the drop-off in supply does NOT mean instant rent rebound. That’ll take time, and other variables (i.e. the job market) will play a role in the pace. But the biggest factor is we still have a large stock of 2024-25 completions still working through prolonged lease-up, trying to get full, and putting downward pressure on rents until they achieve stabilized occupancy.

#apartments #housing #multifamily

Leave a comment