via REM Capital by Robert Ritzenthaler

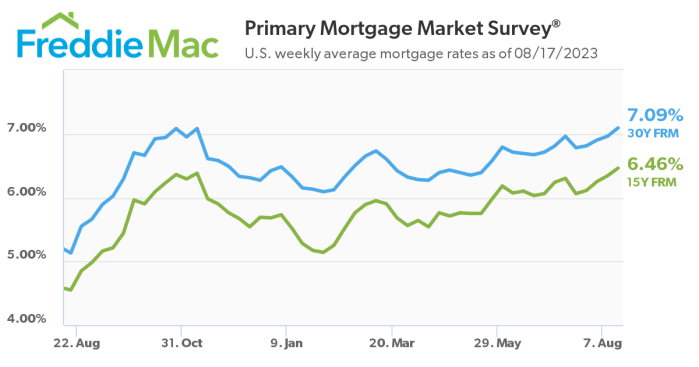

| Jobs Report Shows Weakness Last week’s jobs report reported an unexpected rise in unemployment to 3.8% even as payrolls increased by 187,000. The counts for June and July were revised considerably lower even while average hourly earnings grew by 4.3% year over year. Healthcare added 71,000 jobs for a nice gain – followed by some strength in leisure, hospitality, and construction. Notably, the “real” unemployment rate jumped to 7.1%. These are some of the highest unemployment numbers we’ve seen since before the Fed started hiking rates early last year. From a hiring standpoint, we’ve started to see the pendulum slowly start to swing back in favor of employers. While there are still many folks unemployed for various reasons, many don’t intend to come back into the workforce. Thus we look at the “real” unemployment rate to determine where a good equilibrium lies in overall supply and demand. While we are still seeing pay increases, they are more typical and I think the overall labor market is getting back to a better place. We still have 1.5 jobs per unemployed person, but, not surprisingly, many of those jobs are at the lower end of the scale where our “social net” begins to encourage people to do nothing rather than take a lower paying job. All-in-all, I think the report is a positive sign that the economy is slowing down and that the Fed is closer to achieving a soft landing scenario. If this is true, interest rates should start to drop and credit should start to open up again. The Forward Curve Relative To Fed Expectations When it comes to pricing rate caps, the forward curve is where all the action lies. The forward curve is a combination of expectations of where interest rates will be at some point in the future and where traders are pricing those expectations. If you look at the graph below, you’ll see a bunch of dots representing what different Fed governors think will be the Fed target rate at various points in the future. Here is a link to the latest US Bureau of Labor’s latest job report. —>>> REPORT |

| In short, the majority of Fed governors believe that the target Fed rate will drop 1% per year for the next three years. Interestingly enough, the forward curve, which is essentially how the investment market is pricing those expectations, doesn’t agree. The forward curve is pricing in a 1.5% rate drop and then a leveling off scenario at a much higher interest rate target. While I think it’s wise NOT to fight the Fed, unfortunately our rate cap costs are based on the forward curve so we’re paying for a market that’s disagreeing with the Fed. We’ll see how this plays out over the next 6-12 months. I tend to stick with the Fed consensus which tells me that in a year we’ll be about 1% point lower on Fed Funds target rate. That will open up liquidity and close the gap on the bid/ask spread for multifamily. |

Cap Rates in Orlando, Florida

| Cap Rates as of 09/14/2023 Commercial Property Cap Rates By Property Type, Sector & Class | |||

| Property Type | Class A | Class B | Class C |

| Multifamily Metro Mid & High Rise | 4.75 – 4.85 | 4.85 – 4.95 | 5.00 – 5.45 |

| Multifamily Suburban | 4.85 – 4.95 | 4.95 – 5.05 | 5.20 – 5.70 |

| Retail Metro (CBD) | 6.50 – 7.25 | 6.75 – 7.00 | 7.00 – 7.50 |

| Retail Suburban | 6.20 – 6.90 | 6.70 – 6.80 | 6.90 – 7.40 |

Cap Rate Performance by Asset Class (from Q1 of 2023)

Multifamily – This is the most sought-after commercial property asset classes. Surprisingly, investors only purchased $6.2 billion nationally for apartment building properties in January of 2023, according to Real Capital Analytics. Compare that to the more than $20 billion purchased in January of 2022. Since the third quarter of 2022, this trend from investors has been making it a buyer’s market and expanded cap rates. CBRE states that cap rate expansion started slowing considerably in March of 2023, and should continue at a slower increase though the third quarter of 2023 by about 25 bps.

Dreznin Pappas Commercial Real Estate, LLC

Sean Dreznin * 941.961.8199 * TritonCRE@gmail.com

Leave a comment